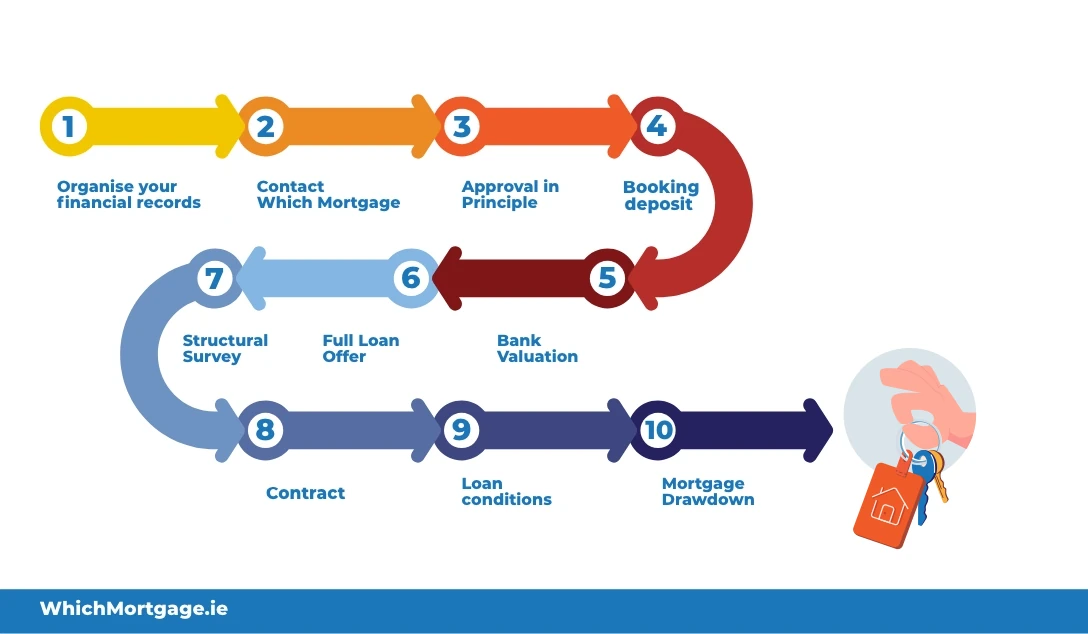

1. Organise your financial records

Before you apply for a mortgage, you will need to show any potential lender that all your bank account statements are in order and that you can support a monthly mortgage repayment. You can demonstrate this with a combination of regular monthly savings, your rent payments or completed loan repayments. You should also pay down credit cards and pay off any loans, if possible.

2. Contact Which Mortgage

There are so many mortgage lenders and mortgage products available it is essential you get the right advice for your particular circumstances. We have the expertise to research the mortgage market for you. See our handy mortgage application checklist which gives you details of the documents you will need to provide in your mortgage application.

3. Approval In Principle

The first step is to apply for an Approval In Principle with the preferred mortgage lender. A fully completed mortgage application is submitted by Which Mortgage and when the mortgage underwriters approve the application an Approval In Principle is issued. This AIP can be obtained without having selected your property. Indeed, Estate Agents and Auctioneers may ask you for sight of your AIP before they will accept a booking deposit on a property.

4. Booking Deposit

When you find the property that you wish to buy you will be asked for a booking deposit by the seller. This deposit holds the property at the agreed price until you receive the Full Loan Offer from the mortgage lender. The deposit is refundable should either party wish to cancel the sale/purchase before contracts are signed.You should employ your solicitor at this stage to begin to address the legal work on your behalf.

5. Bank Valuation

Before the Mortgage Lender issues the Full Loan Offer a bank valuation needs to be carried out. The valuation is paid by you. The Mortgage Lender requires the valuation on the proposed property to assess the value of its security and the rebuilding cost for insurance purposes

6. Full Loan Offer

The Full Loan Offer contains the agreed mortgage amount, the term, the rate and the type of mortgage. It is also sent to your solicitor with the legal documents for your mortgage. You should also receive at this time a “Statement of Suitability” showing the reasons why this mortgage is the best suited to your circumstances.

7. Structural survey

The bank valuation may or may not recommend that you carry out a structural survey on the property. However, it is advisable to engage the experts to make sure that the property is structurally sound and that there are no hidden issues with the construction.

8. Contract

When your solicitor has reviewed the title documents and the purchase contract you will sign the contract itself. You will be asked to pay the remainder of your contribution to the purchase price (less the deposit) and the closing date is agreed.

9. Loan conditions

To close the purchase all the loan conditions outlined in the Full Loan Offer will need to be complied with. These loan conditions usually include; the mortgage protection assurance, the building insurance, the Direct Debit mandate etc

10. Mortgage drawdown

When all the loan conditions are complied with the mortgage lender transfers the mortgage amount to your solicitor, who in turn transfers it to the seller’s solicitor on your behalf. This process is called the draw down of your mortgage. Once these funds have been draw down and have been paid over, you have bought your new home.

All you need to do now is move in!